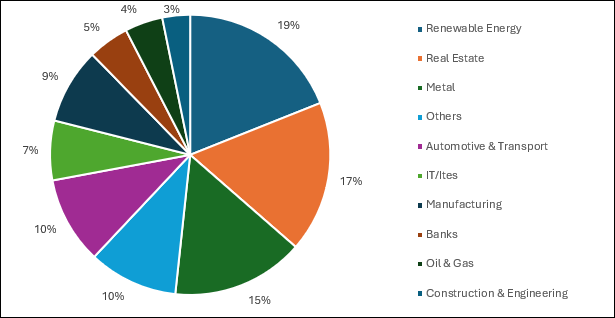

- B/w Jan.-Sept. 2024, Qualified Institutional Placements (QIP) issuance across all sectors scaled a record high of INR 75,923 Cr, with real estate comprising a 17% share – 2nd highest after renewable energy

- 6 developers collectively raised INR 5,275 Cr via IPOs since 2021; Macrotech (Lodha) alone raised nearly INR 2,500 Cr

- Enhanced financial strength boosts developers' launch rate – approx. 13.62 lakh units launched in top 7 cities b/w 2021 to 9M 2024

- Robust sales – approx. 14.36 lakh units sold in this period across top 7 cities; unsold inventory in these cities declined by 10% b/w Q3 2021-end to Q3 2024-end

After the pandemic, Indian real estate developers have been aggressively tapping capital markets through Initial Public Offerings (IPOs) and Qualified Institutional Placements (QIPs). Enhanced transparency, a robust post-pandemic residential real estate recovery, and strong investor confidence are factors driving a surge in activity, thereby positioning the sector for continued growth.

Qualified Institutional Placements allow publicly traded companies to raise capital by offering equities or securities convertible into equity to pre-approved institutional buyers. This fundraising approach lets companies skip the more conventional Initial Public Offering (IPO) route and quickly raise substantial funds.

Anuj Puri, Chairman – ANAROCK Group, says, “ANAROCK's analysis of the available data trends of listed developers on the National Stock Exchange shows that by the third quarter of 2024, the real estate sector contributed over 17% of QIP issuance across sectors, or INR 12,801 Cr of a total of INR 75,923 Cr.”

“After renewable energy, real estate comes in second highest among sectors to raise funds through QIP so far this year,” he says. “This strong QIP activity highlights the sector’s crucial role in India’s broader capital markets – and the institutional investors' growing confidence in Indian real estate.”

Robust housing sales growth after the pandemic has prompted leading developers to unleash relevant inventory across markets. As per ANAROCK Research, over 13.62 lakh units have been launched across the top 7 cities between 2021 to 9M 2024.

Concurrently, housing sales in these cities have soared to approx. 14.36 lakh units in this period. Effervescent sales led to an over 10% decline in unsold housing inventory in this period, despite the high rate of supply addition.

“To fund their aggressive expansion, these developers are turning to IPOs and the QIP route,” says Puri. “Their success in these capitalization efforts underscore the sector’s continued ability to attract both retail and institutional investors. We expect investor participation to grow manifold in the coming years.”

Sector-wise share of QIPs Raised in 9M 2024

Source: NSE & ANAROCK Research

Simultaneously, the strong post-pandemic homebuyers demand has also prompted developers to raise funds via IPOs to fund new project launches across geographies. Since 2021, six developers have collectively raised INR 5,275 Cr through mainstream IPOs. The developers who raised funds via IPOs since 2021 till date are Macrotech Developers Ltd, Shriram Properties, Keystone, Signature Global, Suraj Estate and Arkade Developers.

Among these, Macrotech Developers Ltd. raised the highest of about INR 2,500 Cr.

|

Developers |

Listing Date |

Total Funds Raised (INR Cr) b/w 2021 till Sept. 2024 |

|

Macrotech Developers Ltd. |

19-04-2021 |

2,500 |

|

Sriram Properties |

20-12-2021 |

600 |

|

Keystone |

24-11-2022 |

635 |

|

Signature Global |

27-09-2023 |

730 |

|

Suraj Estate |

26-12-2023 |

400 |

|

Arkade Developers |

24-09-2024 |

410 |

|

Total Mainline IPOs |

|

5,275 |

Source: NSE & ANAROCK Research

Factors Driving IPO & QIP Traction:

- Improved Transparency: The implementation of the Real Estate (Regulation and Development) Act (RERA), Goods and Services Tax (GST), demonetization, etc. have significantly increased transparency in the sector and revived confidence among investors and homebuyers. Developers now adhere to stricter compliance measures, which improves their credibility and makes it easier for them to raise funds in the capital markets.

- Strong Post-Pandemic Recovery: Post-2020, the real estate sector has rebounded strongly, with Grade A developers leading the charge. Market demand for high-quality residential projects has surged, and developers have been quick to capitalize on this with new project launches. By September 2024, the inventory overhang reached its lowest at 14 months, demonstrating how quickly supply is being absorbed by the market.

- Surge in Residential Sales Value: As per ANAROCK Research, in the first nine months of 2024 itself, residential sales value reached INR 4.2 lakh crore – a 22.6% increase over the same period in 2023 and an impressive 115% growth over the total sales value recorded in 2021. This surge in sales value is directly boosting developers' cash flow, allowing them to take on new projects and meet rising demand, further improving investor sentiment.

- Nifty Realty Index Performance: The Nifty Realty Index has surged by nearly 250% between January 2021 and September 2024, making it the second-best performing sector index after the Nifty PSU Bank Index. This growth in the stock market reflects a broader confidence in the real estate sector and its ability to deliver long-term value.

- Institutional Investor Confidence: Institutional investors are increasingly placing their bets on real estate, as evidenced by the rising number of QIP issuances. The record number of QIPs in real estate sector this year (INR 12,801 Cr) underscores the renewed faith that institutional investors have in the sector.